|

1 BAGGAGE AND BONA FIDE BAGGAGE.

Q.1 What is baggage? What articles are treated as bona fide baggage under

Custom Baggage Rules, 1998?

Q.2 Are there any restrictions on import of gifts / souvenirs as

baggage?

Q.3 Can a passenger bring in consumer goods in commercial quantities?

Q.4 Please describe the situations under which a licence is required

for import of goods or articles as baggage

Q.5 How are goods classified that are brought in by a carrier who is

not owner of such goods?

Q.6 What are the applicable rules regarding import of commercial goods

as part of baggage?

Q.7 What are the rules for Declaration & Clearance of Baggage? What are

the consequences of mis-declaration / non-declaration?

2 LEGAL FRAMEWORK

Q.8 What is the legal framework relating to baggage? Explain the

relevant provisions of the Customs Act, 1962

3 DEFINITIONS

Q.9 Kindly explain the definitions of important terms used in the

Custom Baggage Rules, 1998

4 BAGGAGE RULES APPLICABLE TO DIFFERENT CATEGORIES OF PASSENGERS

Q.10 What are the different categories of in-bound passengers?

Q.11 What are the duty free allowances for in-bound Indian Residents

and Foreigners residing in India?

Q.12 What are the duty free allowances for Indian Professionals

returning to India?

Q.13 What are duty free allowances for tourists visiting India?

Q.14 What is transfer of residence? What are duty free allowances for

persons transferring residence?

Q.15 What is the rate of duty applicable on transfer of residence?

Q.16 Whether Foreign nationals, other persons and persons travelling

together are eligible to avail benefits under transfer of residence?

5 APPLICABILITY OF BAGGAGE RULES TO IMPORT OF SPECIFIC ITEMS AS BAGGAGE

Q.17 Can one import Commercial Samples as baggage?

Q.18 What is the value of gifts one can import, duty free, through post

or air freight? .

Q.19 What quantity of Alcoholic Drinks / Cigarettes can be imported as

baggage duty free? What is the applicable Customs duty for imports in

excess of such duty free quantity?

Q.20 How much jewellery can a person returning to India Import free of

duty?

Q.21 Who can import Gold & Silver as baggage? What is the maximum

quantity that can be imported? What is the rate of duty?

Q.22 What are the rules applicable to import of Foreign Exchange /

Currency and to import of Indian Currency?

Q.23 Who can import Fire Arms as baggage? What are the conditions under

which Fire Arms can be imported?

Q.24 Can Pet animals be imported? If so, what are the conditions?

Q.25 How does one deal with Baggage of Deceased Person?

Q.26 What is Unaccompanied Baggage? Are duty free concessions available

for Unaccompanied Baggage?

Q.27 Who can import Passenger Cars? What is the applicable rate of

duty?

Q.28 In what manner do baggage rules apply to Airline Crew? Can members

of crew import laptop into India?

Q.29 What is the General Rate of Customs Duty other than specific rates

on specified articles mentioned above? What are the different types of

Customs Duty?

6 BAGGAGE RULES FOR OUT-BOUND PASSENGERS

Q.30 Are out-going passengers subject to customs clearance? What

articles are prohibited or restricted for export as baggage?

Q.31 What are the requirements for export of gold jewellery through

baggage?

Q.32 Is export of foreign currency & Indian currency permissible, and

if so to what extent?

7 RESTRICTED AND PROHIBITED GOODS

Q.33 Which are the restricted and prohibited goods for import and/or

export?

8 VIOLATIONS AND PENAL PROVISIONS

Q.34 Describe the different types of violations of customs laws and the

penal provisions that are attracted?

9 REFERENCES

10 SUBJECT INDEX

Chapter 1

BAGGAGE AND BONA FIDE BAGGAGE

Q.1 What is baggage? What articles are treated as bona fide baggage under

Custom Baggage rules, 1998?

"Baggage" means possessions or belongings of a person

with which one travels while coming into or going out of the country. Such

baggage could be accompanied or unaccompanied with the person while

travelling. It covers personal and household effects normally carried by

passengers.

Baggage has not been exhaustively defined in the Customs

Act, 1962. Section 2(3) of this Act merely states that baggage includes

unaccompanied baggage but does not include motor vehicles.

Section 79 of the Customs Act, 1962 deals with bona fide baggage exempted

from duty. In exercise of the power given under this section, the Central

Government has notified Custom Baggage Rules, 1998 (as amended from

time-to-time) regulating the rules applicable to a passenger’s baggage

including duty free allowance, levy of custom duty or exemption thereof.

Used personal effects and household or consumer goods

which are generally required by a passenger for satisfying daily necessities

of life are treated as

bona fide baggage. It should be noted that the question of whether the

baggage of a passenger is

bona fide or not would depend on the profile of the passenger. If any

dispute or doubt arises as to ‘bona fide’ nature of

baggage, it should be referred to Addl. / Deputy Collector of Customs who

shall examine the case and take appropriate action (Circular No. 50/95. Cus.

(F.No. 520/127/94-Cus.VI) dt. 18-5-1995).

Q.2 Are there any restrictions on

import of gifts/souvenirs as baggage?

A passenger is allowed to bring in gifts or souvenirs as

baggage. Value of such articles would be covered within the allowances

admissible under the Baggage Rules.

Q.3 Can a passenger bring in consumer goods in commercial

quantities?

Import of consumer goods in commercial quantities is not

permissible under the EXIM policy and is not treated as

bona fide baggage but is

liable to be adjudicated.

Further, where a part of the goods are in commercial

quantity, the entire baggage does not become non- bona

fide and that portion of the baggage which is not in commercial quantity

would be eligible to free baggage allowance (CBEC Circular No. 64/96-Cus. VI

(F.No. 495/6/96-Cus.VI) dt. 17.12.1996).

Q.4 Please describe the situations under which a licence is

required for import of goods or articles as baggage.

A passenger does not need a licence to bring in as

baggage

bona fide

household goods and personal effects which are covered under the Baggage

Rules. These can be imported duty free within the allowances admissible

under the said Baggage Rules. Even if such import exceeds the general free

allowance, no licence is required and it can be released on payment of

applicable duty (as per ITC Public Notice No. 27/80 dt. 15-7-1980 as amended

from time to time).

Goods which are not

bona fide baggage and

therefore not covered by the Baggage Rules would require import licence and

in its absence are liable for confiscation under section 111(8) of the

Customs Act, 1962.

Samples of items that are freely importable under the

EXIM policy may also be imported as part of a passenger’s baggage without a

licence or permission but subject to duty free allowances admissible under

the Baggage Rules.

Exporters coming from abroad are allowed to import

drawings, patterns, labels, price tags, embellishments, etc. as part of

their baggage without licence/certificate / permission provided these are

intended to be taken back on their departure from India.

Q.5 How are goods classified that are brought in by a

carrier who is not owner of such goods?

Goods brought through a person who is merely acting as a

carrier cannot be classified as ‘gifts’ or as ‘personal baggage’ of the

carrier but would be classified as imported goods requiring a valid import

licence (Saroj Goenka

vs. Collector of Customs, Madras 1987 (13) ECR 585 (CEGAT

SRB)).

Q.6 What are the applicable rules regarding import of

commercial goods as part of baggage?

Commercial goods which can be freely imported as normal

cargo either by air or sea can be brought as part of a passenger’s baggage.

However, if any restrictions and prohibitions have been specified in import

policy of goods, they would be applicable, irrespective of whether the items

are brought by air, sea or baggage. As regards rate of duty, such commercial

imports would be assessed to duty at the baggage rate and not under their

respective headings (Ministry of Finance No. 495/10/1992-96-Cus/VI dt.

7-7-1992).

Q.7 What are the rules for Declaration & Clearance of

Baggage? Describe Green Channel and its use. What are the consequences of mis-declaration

/ non-declaration?

The owner of the baggage is required under section 77 of

the Customs Act, 1962, to make declaration of its contents to the proper

officer of customs, for the purpose of clearing it. The Central Board of Excise & Customs, in

exercise of the powers under section 81, has prescribed a form, known as

Baggage Declaration Form, for declaring the contents of the baggage.

If a passenger has nothing to declare to the Customs and

is carrying dutiable goods within the prescribed duty free allowance, he/she

can simply walk through the exit marked Green Channel with their baggage on

the basis of their Oral Declaration/Declaration on their Disembarkation

Card, without any other question being asked by Customs.

Non-declaration, mis-declaration and concealment of

imported goods is an offence under the Customs Act, which may result in

confiscation of goods imported, fines, penalties and even prosecution. In

case of Non-declaration, the passenger cannot subsequently claim the benefit

of temporary detention of the goods as available u/s 80 as described in the

relevant provisions of the Customs Act, 1962 hereinafter. Normally goods are

detained for purposes of nonpayment of duty, shortage of exchange etc.

Chapter 2

LEGAL FRAMEWORK

Q.8 What is the legal framework relating to baggage?

Explain the relevant provisions of the Customs Act, 1962

Sections 77 to 81 of the Customs Act, 1962 contains

provisions applicable to baggage of passengers. These are:

-

As per section 77, the owner of baggage is required

to make a full declaration of its contents to the proper officer for the

purpose of clearing it. Thus onus is cast on the passenger to make a full

and true declaration. Any dutiable or prohibited goods which are not

declared or are in excess of those included in the declaration can be

confiscated by the Customs authorities under section 111 of the Customs

Act.

-

Section 78 deals with determination of rate of duty

and tariff valuation. It provides that the rate and valuation in force on

the date on which a declaration is made in respect of such baggage shall

be the applicable rate. The general rate of duty for items imported in

excess of the permissible free allowance is 35%

ad valorem + 3%

education cess i.e. an effective rate of 36.05%.

Section 79 provides for bona fide baggage to be

exempted from duty as per rules that the Central Govt. is empowered to

make for the purpose. Such rules may specify, inter alia, the minimum

period for which article has been used by passenger, maximum value of any

individual article and maximum total value of all articles which may be

passed free of duty.

Section 80 deals with temporary detention of

baggage. It is applicable, at the request of the

passenger, either to an article which is dutiable

or an article whose import is prohibited provided a true declaration

has been made by the passenger under section 77. The passenger can

request for temporary detention of the article until it is returned

to him on his leaving India. If for any reason the passenger is not

able to collect the article at the time of his leaving India, the

article may be returned to him through any other passenger

authorized by him and leaving India or as cargo consigned in his

name. The following are some examples of situations where a

passenger may decide to keep his articles in custody of Customs:

-

He does not have sufficient money or

foreign currency to pay duty at that moment.

-

He does not want to take the article into

India but intends to return with it when leaving India.

-

He disputes the valuation/duty as

determined by the Customs officer and wishes to appeal to higher

authorities against the valuation/duty.

-

The articles are prohibited goods and he

has declared them to the Customs officer. It should be noted

that all prohibited goods cannot be kept in safe custody in this

manner as banned items such as narcotics, pornographic items,

etc. are liable to seizure and confiscation.

-

Section 81 empowers the Board to make

regulations providing for (i) the manner of declaring contents

of any baggage, (ii) the custody, examination, assessment to

duty and clearance of baggage and (iii) the transit or

transshipment of baggage from one customs station to another or

to a place outside India

Chapter 3

DEFINITIONS

Q.9 Kindly explain the definitions of important terms

used in the Custom Baggage Rules, 1998

Relevant definitions under the Baggage Rules, 1998

as amended from time-to-time are as under:

Section 2(ii): "resident" means a person holding a

valid passport issued under the Passports Act, 1967 (15 of 1967) and

normally residing in India;

Section 2(iii): "tourist" means a person not

normally resident in India, who enters India for a stay of not more

than six months in the course of any twelve months period for

legitimate non-immigrant purposes, such as touring, recreation,

sports, health, family reasons, study, religious pilgrimage or

business;

Section 2(iv): "family" includes all persons who

are residing in the same house and form part of the same domestic

establishment;

Section 2(v): "professional equipment" means such

portable equipments, instruments, apparatus and appliances as are

required in his profession, by a carpenter, a plumber, a welder, a

mason, and the like and shall not include items of common use such as

cameras, cassette recorders, dictaphones, personal computers,

typewriters, and other similar articles.

Chapter 4

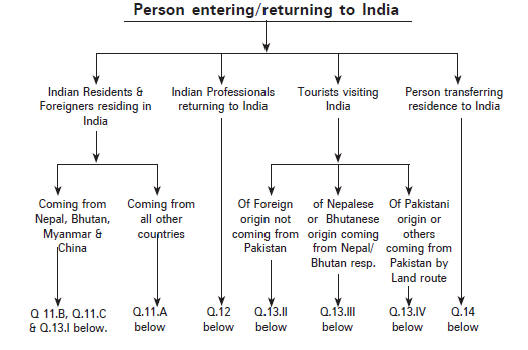

BAGGAGE RULES APPLICABLE TO DIFFERENT CATEGORIES OF PASSENGERS

Q.10 What are the different categories of in-bound

passengers?

Baggage rules are applicable to all categories of

passengers having different purposes like (i) business, (ii) tourism and

(iii) Transfer of Residence and whether Indian Resident or not. Under these

rules, duty free allowances are provided to different categories of

passengers depending upon the purpose, duration of travel/stay at the

destination, age, and/or place from where they are coming.

The following chart gives an overview of the different

categories of in-bound passengers and the applicable Question No. s under

which the relevant duty free allowances are listed:

Q.11 What are the duty free allowances for in-bound Indian

residents and foreigners residing in India?

As referred in important definitions earlier, a Resident

means a person holding a valid passport issued under the Passports Act, 1967

and normally residing in India. Duty free clearances are available to

returning Residents as well as to returning Foreigners who are residing in

India under Rules 3 and 4 of the Baggage Rules, 1998. Details of these

allowances are as under:

-

Passengers coming from countries other than Nepal,

Bhutan, Myanmar and China:

|

Duty free allowance for bona fide baggage consisting of

|

For passengers of age

|

|

|

10 years and above

|

Below 10 years

|

|

(i) Used personal effects, excluding Free Free jewellery, required for

satisfying daily necessities of life

|

|

|

|

(ii) Articles other than those mentioned in Annex. I (given below) if

carried in person or in the accompanied baggage of the passenger

|

|

|

|

(a) if stay abroad for more than three days |

Valued up to

25,000/-

|

Valued up to

6,000/-

|

|

(b) If stay abroad up to three days |

Valued up to

12,000/- |

Valued up to

3,000/-

|

-

Passengers coming from Nepal, Bhutan, Myanmar and

China OTHER than by land route:

|

Duty free allowance for bona fide baggage consisting of

|

For passengers of age

|

|

|

10 years and above

|

Below 10 years

|

|

(i) Used personal effects, excluding jewellery, required for

satisfying daily necessities of life

|

Free |

Free |

|

(ii) Articles other than those

mentioned

in Annex I (given below) if carried

in person or in the accompanied

baggage of the passenger |

|

|

|

(a) if stay abroad for more than three

days |

Valued up to

6,000/- |

Valued up to

1,500/- |

|

(b) If stay abroad up to three days |

Nil

|

Nil |

-

Passengers coming from Nepal, Bhutan, Myanmar and

China BY land route:

|

Duty free allowance for

bona

fide baggage consisting of

|

For passengers of age |

|

|

10 years and above |

Below 10 years

|

|

(i) Used personal

effects, excluding jewellery, required for

satisfying daily necessities of life.

|

Free |

Free |

|

(ii) Articles other

than those mentioned in Annex I (given below) if carried in person or in

the accompanied baggage of the passenger |

Nil

|

Nil

|

Notes:

-

Used personal effects, excluding jewellery are those

that are required for satisfying daily necessities of life. It has not been

defined in the Baggage Rules and the Customs officer exercises his judgment

in deciding the nature of the articles. The following are illustrative

examples: used clothes such as shirts, trousers, jeans, frocks, etc. and

other items of personal wear; used toiletries & cosmetics; used footwear,

used bedding, shaving kits, spectacles, hearing aid, etc. However, it should

be noted that electronic items, household durables or ‘white goods’ and

furniture cannot be classified as personal effects.

-

Free allowance cannot be pooled with the free

allowance of any other passenger such as members of family or group travelling together. Each passenger is considered to be travelling

separately and his duty is assessed on an individual basis and not on the

basis of a group or a family.

-

Goods over and above the free allowances shall be

chargeable to customs duty @ 35% + Education cess of 3% i.e. at effective

rate of 36.05%

-

Annexure 1 (referred in the tables above) refers to

articles that are not eligible for duty free allowance in excess of the

limits specified under it. Articles specified therein are as follows:

-

Fire arms

-

Cartridges of fire arms exceeding 50

-

Cigarettes exceeding 200 or cigars exceeding 50 or

tobacco exceeding 250 gms

-

Alcoholic liquor or wines in excess of 2 litres

-

Gold or silver, in any form, other than ornaments

-

One laptop computer (notebook computer) over and above

the said free allowances mentioned above is also allowed duty free if

imported by any passenger of age 18 years and above.

-

In case the value of one item exceeds the duty free

allowance, the duty shall be calculated only on the excess of such amount.

-

Annexure IV specifies the Customs stations for those

passengers who enter India by Land route as mentioned in the tables above.

These are:

Amritsar

(i) Amritsar Railway Station

(ii) Attari Road

(iii) Attari Railway Station

(iv) Khalra

Vadodara

(v) Assara Naka

(vi) Khavda Naka

(vii) Lakhpat

(viii) Santalpur Naka

(ix) Suigam Naka

Delhi

(x) Delhi Railway Station

Ferozpur District

(xi) Hussainiwala

Jodhpur Division

(xii) Barmer Railway Station

(xiii) Munabao Railway Station

Baramullah District

(xiv) Adoosa

Poonch District

(xv) Chakan-da-bagh

Q.12 What are the duty free allowances for Indian

professionals returning to India?

An Indian passenger who was engaged in his profession

abroad is allowed, on his return to India, additional duty free allowance on

his baggage under Rule 5 of the Baggage Rules, 1998 to the extent as

mentioned below. These allowances are in addition to the allowances

available to in-bound residents under Rules 3 & 4 covered earlier under Q.11

|

(a) |

Indian passenger returning after at least 3 months

|

(i) Used household articles (such as linen, utensils,

tableware, kitchen, appliances and an iron) up to an aggregate value of

12000/-

(i) Professional equipment up to a value of

20,000/-

|

|

(b)

|

Indian passenger returning after at least 6 months

|

(i) Used household articles (such as linen, utensils,

tableware, kitchen, appliances and an iron) up to an aggregate value of

12,000/-

(ii) Professional equipment up to a value of

40,000/-

|

|

(c) |

Indian passenger returning after a stay of a minimum of

365 days during the preceding two years on termination of his work and who has

not availed this concession in the preceding three years

|

Used household articles and personal effects (which have been

in the possession and use abroad of the passenger or his family for at least six

months) and which are not mentioned in Annex. I, Annex. II & Annex. III up to an

aggregate value of 75,000/-

|

This concession is not available to passengers who were

merely on training abroad. However, those Govt. officials who are deputed on

training abroad are entitled to this concession.

In case of professionals returning on termination of their work as per Para

(c) above, concession up to 75,000 is available on used household

articles and personal effects which have been in possession and used abroad by

the passenger/his family for at least 6 months provided they are not covered in

Annexures I, II & III. Unutilized portion, if any, of 75,000 may be available for importing

items under Annexure II or Annexure III.

Articles listed under Annexure III are allowed duty free

for one unit each and articles listed at Annexure II are allowed to be

imported at a concessional rate of duty of 15.45% for one unit each, within

the above-mentioned value ceiling.

Annexure I (mentioned in the table above) refers to articles

that are not eligible for duty free allowance in excess of the limits specified

under it. Articles specified therein are as follows:

-

Fire arms

-

Cartridges of fire arms exceeding 50

-

Cigarettes exceeding 200 or cigars exceeding 50 or

tobacco exceeding 250 gms

-

Alcoholic liquor or wines in excess of 2 litres

-

Gold or silver, in any form, other than ornaments

Annexure II (mentioned in the table above) specifying

articles on which concessional rate of duty of 15.45% is available for one unit

each is as under:

-

Colour Television or Monochrome Television

-

Digital Video Disc Player

-

Video Home Theatre System

-

Dish Washer

-

Music System

-

Air Conditioner

-

Domestic refrigerators of capacity above 300 litres

or its equivalent

-

Deep Freezer

-

Microwave Oven

-

Video camera or the combination of any such video

camera with one or more of the following goods, namely:–

a. Television Receiver

b. Sound recording or reproducing apparatus

c. Video reproducing apparatus

-

Word Processing Machine

-

Fax Machine

-

Portable Photocopying Machine

-

Vessel

-

Aircraft

-

Cinematographic films of 35 mm and above

-

Gold or silver, in any form, other than ornaments

Annexure III (mentioned in the table above) specifying

articles on which duty free concession is available for one unit each is as

under:

-

VCR or VCP or VTR or VCDP

-

Washing Machine

-

Electrical or LPG Cooking Range

-

Personal Computer (Desktop Computer)

-

Lap Top Computer (Notebook Computer)

-

Domestic Refrigerator up to 300 ltr. capacity or its

equivalent

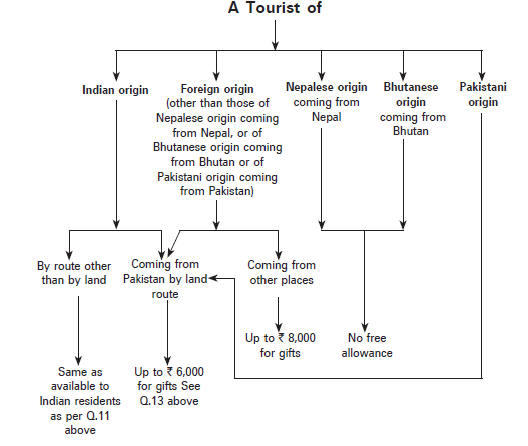

Q.13 What are duty free allowances for tourists visiting

India?

A tourist arriving in India is allowed to clear goods free of duty to the

extent as mentioned in Rule 7 of the Baggage Rules, 1998 if such goods/articles

form part of his/ her

bona

fide baggage. Provisions distinguish between tourist of Indian origin and

Foreign origin; Foreign origin is further divided into those from Nepal, Bhutan

and Pakistan and those of other than these three countries. Tourist of Indian

origin or Foreign origin returning from or coming from Pakistan by land route is

distinguished separately. Duty free allowances for a tourist are as under:

|

|

Articles allowed free of duty

|

|

I

|

Tourists of Indian origin other than those coming from

Pakistan by land route

|

(i) Used personal effects and travel souvenirs, if –

(a) These goods are for personal use of the tourist, and

(b) These goods, other than those consumed during the

stay in India, are re-exported when the tourist leaves India for a foreign

destination

(ii) duty free allowances applicable to Indian Residents as

covered at Q.11 above

|

|

II |

Tourists of foreign origin other than those of Nepalese

origin coming from Nepal or of Bhutanese origin coming from Bhutan or of

Pakistani origin coming from Pakistan

|

(i) Used personal effects and travel souvenirs, if

(a) These goods are for personal use of the tourist, and

(b) These goods, other than those consumed during the

stay in India, are re-exported when the tourist leaves India for a foreign

destination

(ii) Articles up to a value of

8,000/- for making gifts

|

|

III

|

Tourists of Nepalese origin coming from Nepal or of

Bhutanese origin coming from Bhutan

|

No free allowance. |

|

IV

|

Tourists of Pakistani origin or foreign tourists coming

from Pakistan or tourists of Indian origin coming from Pakistan by land route

|

(i) Used personal effects and travel souvenirs, if

(a) These goods are for personal use of the tourist, and

(b) These goods, other than those consumed during the

stay in India, are re-exported when the tourist leaves India for a foreign

destination.

(ii) Articles up to a value of

6,000 for making gifts

|

The above may be depicted by way of chart as under:

Q.14 What is transfer of residence? What are duty free

allowances for persons transferring residence?

Transfer of Residence (TR) is a facility provided to

every person who is coming to India for or by way of transfer of his / her

residence after a stay abroad of at least two years. Such person could be

either (i) an Indian, (ii) a Foreign passport holder, (iii) a minor, or (iv)

a student. This facility allows the person and his/her family to import

personal and household articles free of duty and certain other listed items

on payment of a concessional rate of duty.

Such a person who is transferring his residence to India

is allowed additional duty free allowance on his baggage

under Rule 8 of the Baggage Rules, 1998 to the extent and

subject to the conditions as mentioned below. These allowances are in

addition to the allowances available to in-bound residents under Rules 3 & 4

covered earlier under Q. 11

|

Articles allowed free of duty |

Conditions |

Relaxation that may be considered

|

|

(a) Used personal and household articles other than those

listed at Annexure I or Annexure II, but including the articles listed at

Annexure III, and

Jewellery up to

10000 by a gentleman passenger or

20000 by a lady passenger

Import of Articles listed at Annexure II will be subjected to

concessional rate of duty.

|

(1) Minimum stay of two years abroad, immediately

preceding the date of his arrival on transfer of residence

(2) Total stay in India on short visits during the 2

preceding years should not exceed 6 months, and

(3) Passenger has not availed this concession in the

preceding three years

|

(a) For condition (1): Shortfall of up to 2 months in stay

abroad can be condoned by Deputy/Assistant Commissioner of Customs if the

early return is on account of

(i) terminal leave or vacation being availed of by the

passenger, or

(ii) any other special circumstances

(b) For condition (2): Commissioner of Customs may condone

short visits in excess of 6 months in deserving cases

(c) For condition (3): No relaxation

|

|

(b) Jewellery taken out earlier by the passenger or by a

member of his family from India

|

Satisfaction of the Assistant Commissioner of Customs

regarding the jewellery having been taken out earlier from India

|

|

If both husband and wife working abroad are transferring

their residence to India, both may avail the concessions available on

individual basis on satisfaction of conditions. However, benefit will not be

available to each one of them when they were having common establishment and

staying in the same house abroad.

Q.15 What is the rate of duty applicable on transfer of

residence?

Duty free import as baggage is allowed under TR of used

personal articles and household effects including items listed at Annexure I

(up to limits specified therein) and Annexure III. In addition to that, the

usual allowances applicable to returning Indian residents or foreigners

residing in India under Rules 3 & 4 of the Baggage Rules (as per Q. 11

above) are also available to passengers availing TR. However, articles

listed in Annexure II of the Baggage Rules are dutiable and do not comprise

articles allowed duty free as household effects. Clearance of such items

listed in Annexure-II, whether old or new, is allowed at a concessional rate

of duty of 15% ad

valorem + 3% educational cess.

Annexure I (mentioned above) refers to articles that are not

eligible for duty free allowance in excess of the limits specified under it.

Articles specified therein are as follows:

-

Fire arms

-

Cartridges of fire arms exceeding 50

-

Cigarettes exceeding 200 or cigars exceeding 50 or

tobacco exceeding 250 gms

-

Alcoholic liquor or wines in excess of 2 litres

-

Gold or silver, in any form, other than ornaments

Annexure II (mentioned above) specifying articles on which

concessional rate of duty of 15.45% is available for one unit each is as under:

-

Colour Television or Monochrome Television.

Digital Video Disc Player.

Video Home Theatre System.

Dish Washer.

Music System.

Air Conditioner.

Domestic refrigerators of capacity above 300 litres

or its equivalent.

Deep Freezer.

Microwave Oven.

Video camera or the combination of any such video

camera with one or more of the following goods, namely:–

a. Television Receiver;

b. Sound recording or reproducing apparatus;

c. Video reproducing apparatus.

Word Processing Machine.

Fax Machine.

Portable Photocopying Machine.

Vessel.

Aircraft.

Cinematographic films of 35 mm and above.

Gold or silver, in any form, other than ornaments.

Conditions for Annexure II items

-

Passenger to affirm by a declaration that such goods

have been in his/her possession abroad or the goods are purchased from the

duty-free shop by him/her at the time of his/her arrival but before

clearance from Customs.

-

Only one unit of each item per family is allowed and

total value of these items along with items listed at Annexure III of the

Baggage Rules should not exceed

5 lakhs.

Unaccompanied goods must be shipped or despatched

and arrive in India within the prescribed time limits under the Baggage

Rules, 1998 (within two months before arrival and within after one month of

arrival).

Only one unit of each item will be allowed under TR.

If more than one unit is brought, the excess unit(s) will be classified as

general baggage in which case the usual rate of baggage duty of 36.05%

(after deduction of the free allowance from the total value of all such

items) will be applicable. Similarly, if the total value of the above

Annexure II items and Annexure III items described before exceed

5 lakhs, then the item(s) due to

which the value is exceeding the ceiling amount must be brought as a general

baggage item.

Annex. III (mentioned above) specifying articles which are

allowed free of duty under TR is as under:

-

VCR or VCP or VTR or VCDP

-

Washing Machine

-

Electrical or LPG Cooking Range

-

Personal Computer (Desktop Computer)

-

Lap Top Computer (Notebook Computer)

-

Domestic Refrigerator up to 300 ltr. capacity or its

equivalent.

Conditions for Annexure III items

-

Passenger to affirm by a declaration that such goods

have been in his/her possession abroad or the goods are purchased from the

duty-free shop by him/her at the time of his/her arrival but before

clearance from Customs.

-

Only one unit of each item per family is allowed and total value of these

items along with items listed at Annexure II of the Baggage Rules should not

exceed

5 lakhs.

Unaccompanied goods must be shipped or despatched

and arrive in India within the prescribed time limits under the Baggage

Rules, 1998 (within two months before arrival and within after one month of

arrival).

Only one unit of each item will be allowed under TR.

If more than one unit is brought, the excess unit(s) will be classified as

general baggage in which case the usual rate of baggage duty of 36.05%

(after deduction of the free allowance from the total value of all such

items) will be applicable. Similarly, if the total value of the above

Annexure III items and Annexure II items described before exceed

5 lakhs, then the item(s) due to

which the value is exceeding the ceiling amount must be brought as a general

baggage item.

Q.16 Whether Foreign nationals, other persons and persons travelling together are eligible to avail benefits under transfer of

residence?

-

The concessions under TR are available to Foreign

Nationals also.

-

Indian Diplomat returning to India before two years

stay abroad can avail the concession if he has returned for official

reasons, subject to certificate from Ministry of External Affairs to this

effect.

-

Minors are eligible for this concession.

-

TR concession for family members staying together is

not available in case of each member unless it can be established that

persons are working / staying separately.

-

Persons coming from Nepal & Bhutan do not require

passport & visa. Such passengers travelling from Nepal or Bhutan for bona fide transfer of

residence can claim TR concession provided certificates about their bona fide transfer is

issued by the authorized officers in the embassy.

Chapter 5

APPLICABILITY OF BAGGAGE RULES TO SPECIFIC ITEMS AS BAGGAGE

Q.17 Can one import Commercial Samples as baggage?

It is possible for a commercial traveller and businessmen

to import such samples as personal baggage or import by post or air free of

custom duty if (a) these goods are marked as samples, not exceeding

300,000 in value and 15 in numbers

within a period of last 12 months, (b) the importer makes certain

declaration and undertaking and (c) produces his Import Export Code Number.

In case of import of samples relating to gem and

jewellery industry imported by exporters of gem and jewellery, the exemption

shall be 300,000 or 0.25% of average value

of three immediately preceding years’ export, whichever is lower.

Exemption granted shall not exceed

10,000 in case import is by

courier/post/in aircraft.

Q.18 What is the value of gifts one can import, duty free,

through post or air freight?

One can import bona fide gifts by post or

as air freight, up to 10,000 without payment of duty.

Q.19 What quantity of Alcoholic Drinks/Cigarettes can be

imported as baggage duty free? What is the applicable Customs duty for imports

in excess of such duty free quantity?

Following quantities of Alcoholic drinks and Tobacco products are allowed for

import within the duty free allowances admissible to various categories of

incoming passengers:

-

Alcoholic liquors or Wines up to 2 litres

-

200 Cigarettes or 50 Cigars or 250 gms tobacco.

The rate of duty applicable on these products over and

above the above-mentioned free allowance is as under:

-

Cigarettes: Basic Custom Duty ("BCD") @100% +

education cess @ 3%

-

Whisky: BCD @150% + Additional Custom Duty ("ACD")

@ 4% + education cess @3%

-

Wines and Beer: BCD @100% + ACD Nil + education

cess @ 3%

Q.20 How much jewellery can a person returning to India

Import free of duty?

A non-tourist passenger of Indian origin who has been

residing abroad for over one year is allowed to bring jewellery, free of

duty in his bona fide

baggage up to an aggregate value of

10,000/- (in the case of a male

passenger) or 20,000/- (in the case of a

lady passenger). No distinction has been made between adult and minor

passengers.

If a person has taken jewellery out of India at the time

of their departure, its import would be allowed free of duty on production

of Jewellery Export Certificate and provided it is proved to the

satisfaction of Assistant Commissioner of Customs.

Q.21 Who can import Gold and Silver as baggage? What is the

maximum quantity that can be imported? What is the rate of duty?

Gold and silver can be imported as baggage by:

-

any passenger of Indian Origin (even if he is a

foreign national except Pakistani/Bangladeshi national), or

-

a passenger holding a valid passport, issued under

the Passport Act, 1967,

who is coming to India after a period of not less than

six months of stay abroad; and short visits, if any, made by the passenger

during the aforesaid period of six months shall be ignored if the total

duration of stay on such visits does not exceed thirty days.

Other conditions are:

-

The duty shall be paid in convertible foreign

currency.

-

The weight of gold (including ornaments) should not

exceed 10 kgs. per passenger. The weight of silver (including ornaments)

should not exceed the quantity of 100 kgs. per passenger.

-

The passenger should not have brought gold or other

ornaments during any of his visits (short visits) in the last six months

i.e. he has not availed of the exemption under this scheme, at the time of

short visits.

-

Ornaments studded with stones and pearls are not

allowed to be imported.

-

The passenger can either bring the gold or silver

himself at the time of arrival or import the same within fifteen days of his

arrival in India as unaccompanied baggage.

-

The passenger can also obtain the permitted quantity of gold or silver

from Customs bonded warehouse of State Bank of India and Metals and Minerals

Trading Corporation subject to conditions (i) and (ii) above. He is required to

file a declaration in the prescribed Form before the Customs Officer at the time

of arrival in India stating his intention to obtain the gold from the Customs

bonded warehouse and pay the duty before clearance.

|

S.No.

|

Description of Goods |

Rate

|

|

1

|

Gold bars, other than tola bars, bearing manufacturers or

refiners engraved serial number and weight expressed in

metric units and gold coins |

`

300 per 10 gms.+ 3% Education Cess |

|

2

|

Gold in any form other than at Sl. No. 1 above including tola

bars and ornaments, but excluding ornaments studded with

stones or pearls

|

`

750 per 10 gms. + 3% Education Cess

|

|

3

|

Silver

|

`

1,500 per kg. + 3%

Education Cess

|

Note: Only such jewellery, which is in addition to the

jewellery otherwise allowed without payment of duty, is liable to payment of

duty under the above-mentioned scheme of import of gold.

The Scheme for import of Gold & Silver does not provide for

establishing source of such investments for the purpose of import. Therefore

concerned custom officer cannot make such enquiry. However it is pertinent to

note that Import duty is payable only in convertible foreign currency. Therefore

currency purchase endorsement on passport may be enquired upon, except under

certain imports where duty payment is permitted in Rupees.

Q.22 What are the rules applicable to import of Foreign

Exchange/Currency and to import of Indian Currency?

Any person can bring into India from a place outside

India foreign exchange without any limit. However, declaration of foreign

exchange/currency is required to be made in the prescribed Currency

Declaration Form in the following cases:–

i. Where the value of foreign currency notes exceeds US

$ 5,000/- or equivalent

ii. Where the aggregate value of foreign exchange (in

the form of currency notes, bank notes, traveller cheques etc.) exceeds US

$ 10,000/- or its equivalent

Import of Indian Currency is prohibited. However, in the

case of passengers normally resident in India who are returning from a visit

abroad, import of Indian Currency up to

7,500 is allowed.

Q.23 Who can import Fire Arms as baggage? What are the

conditions under which Fire Arms can be imported?

Import of firearms is strictly prohibited. Import of

cartridges in excess of 50 is also prohibited.

However, in the case of persons transferring their

residence (as per conditions specified in the rules) to India for a minimum

period of one year, one firearm of permissible bore can be allowed to be

imported subject to the conditions that:

i. the same was in possession and use abroad by the

passenger for a minimum period of one year and also subject to the

condition that such firearm, after clearance, shall not be sold, loaned,

transferred or otherwise parted with, for consideration or otherwise,

during the lifetime of such person;

ii. the passenger has a valid arms licence from the

local (Indian) authorities;

iii. the customs and other duties as applicable shall

be paid. Presently, customs duty payable on import of firearms is 50% ad valorem (i.e.

based on value) as per Notification No. 106/2008 dt. 22-9-2008

Q.24 Can pet animals be imported? If so, what are the

conditions?

Domestic pets like dogs, cats, birds, etc. are permitted to be imported. A

passenger may import pets (dog and cat only) up to two numbers only at one time

subject to production of required health certificate from country of origin and

examination of the said pets by the concerned quarantine officer. Imports of

pets over and above this quantity shall be allowed only against an Import

sanitary

permit issued by the department of animal husbandry and

dairying or against an import licence issued by the DGFT.

Q.25 How does one deal with Baggage of Deceased Person?

Used,

bona fide personal and household effects belonging to a deceased

person are allowed to be imported free of duty subject to the condition that

a Certificate from the concerned Indian mission (Embassy/High Commission) is

produced at the time of clearance regarding the ownership of the goods by

the deceased person.

Q.26 What is Unaccompanied Baggage? Are duty free

concessions available for Unaccompanied Baggage?

Articles of baggage which could not be brought by a

passenger along with him but which are sent through cargo is treated as

unaccompanied baggage. No free allowance is admissible in case of

unaccompanied baggage which is chargeable to Customs duty @ 35% ad valorem

+ 3%

Education Cess. Only used personal effects can be imported free of duty. The

following important aspects regarding unaccompanied baggage should be noted:

-

Provisions of Baggage Rules are also extended to

unaccompanied baggage except where they have been specifically excluded.

-

The unaccompanied baggage should be in the

possession abroad of the passenger and shall be dispatched within one

month of his arrival in India or within such further period as the

Deputy/Assistant Commissioner of Customs may allow.

-

The unaccompanied baggage may land in India up to

two months before the arrival of the passenger or within such period, not

exceeding one year as the Deputy/Assistant Commissioner of Customs may

allow, for reasons to be recorded, if he is satisfied that the passenger

was prevented from arriving in India within the period of two months due

to circumstances beyond his control, such as sudden illness of the

passenger or a member of his family, or natural calamities or disturbed

conditions or disruption of the transport or travel arrangements in the

country or countries concerned on any other reasons, which necessitated a

change in the travel schedule of the passenger.

Q.27 Who can import Passenger Cars? What is the applicable

rate of duty?

Passenger Cars/Jeeps/Multi-utility vehicles, etc. can be

imported by passengers coming to India only on Transfer of Residence.

The following rates of Duty are applicable for import of

motor cars and other motor vehicles principally designed for the transport

of persons including station wagons and racing cars. Since motor vehicles

are excluded from the definition of Baggage, duties are collected at the

Tariff rate taking into consideration exemption notifications if any.

Customs duty for vehicles which had been registered

abroad

|

Vehicle |

Basic Duty |

Addl. Duty |

Total Duty

|

|

Cars |

105% |

24.72% #

|

160.35% #

|

|

Motor cycles/scooters/ moped |

105% |

16.48% #

|

142.95% #

|

Customs duty for vehicles which had not been registered

abroad

Vehicle Basic Duty Addl. Duty Total Duty

|

Vehicle |

Basic Duty |

Addl. Duty |

Total Duty

|

|

Cars |

60% ** |

24.72% # |

102.54% #

|

|

Motor cycles/scooters/ moped |

60% ** |

16.48% # |

88.96% # |

** if brought in Completely Knocked Down (CKD)

condition, Basic Duty will be 20%.

# Inclusive of Education Cess of 3% imposed as per

Finance Act, 2008.

These imports shall be subject to the condition that the

vehicle should have right hand steering and controls (applicable on vehicles

other than 2 and 3 wheelers)

Value of these vehicles for the purpose of levy of

customs duty is CIF value, where C stands for the cost of the goods, I is

the insurance and F is the freight. Cost in the case of new vehicle is the

transaction value between the seller and the buyer. However, in the case of

old and used vehicles, cost is arrived at by taking value of the new vehicle

in its year of manufacture and then allowing depreciation at following

rates:

-

For every quarter during 1st year – 4%

-

For every quarter during 2nd year – 3%

-

For every quarter during 3rd year – 2.5%

-

For every quarter during 4th year – 2% subject to

a max. depreciation of 70% and thereafter

Q.28 In what manner do baggage rules apply to Airline Crew?

Can members of crew import laptop into India?

As per Rule 10 of the Baggage Rules, the members of the

crew engaged in foreign-going vessels are not considered as tourists or

returning Indians and therefore duty free allowance available in various

rules is not available to them every time when they return to India.

Crew members are required to submit the correct

declaration before Custom authorities with respect to currency, gold

ornaments and electronic goods, etc. in their possession on arrival as well

as departure.

Crew members are allowed to bring items like chocolates,

cheese, cosmetics and other petty gift items for their personal or family

use up to a value of

600 only at the returning of the

aircraft from foreign journey. However, a crew member on final pay off or at

the termination of his engagement with the Airline shall be eligible for

allowances as a common passenger.

The permission given to passengers of age 18 years or

more to bring one laptop without payment of duty on arrival into India is

not available to members of crew arriving in India.

Q.29 What is the General Rate of Customs Duty other than

specific rates on specified articles mentioned above? What are the different

types of Customs Duty?

i. Generally, items imported as baggage are subjected to

a uniform rate of duty for ease of assessment.

ii. The general rate of duty for items imported in excess

of the permissible free allowance is 35% ad valorem

+

educational cess @ 3% i.e. to say that effective rate of duty is 36.05%.

iii. The rate of duty applicable to items in Annexure II

imported by passengers transferring their residence or returning to India

after a stay of 365 days abroad in the preceding two years is 15% +

educational cess @ 3%

Apart from basic customs duty, other types of customs

duty are Additional Duty and Special Additional Duty. Customs duty is levied

on imported goods to bring its landed cost in-line with Indian manufactured

goods so as to retain competitiveness of Indian industries. In this sense,

customs duty is similar to excise duty levied on Indian manufactured goods.

Goods brought in as baggage are specifically exempted from Additional Duty

and Special Additional Duty. However, Education Cess @ 3% is levied on the

customs duty charged on the goods brought in as baggage and not on the basic

value of the goods.

Chapter 6

BAGGAGE RULES FOR OUT-BOUND PASSENGERS

Q.30 Are out-going passengers subject to customs clearance?

What articles are prohibited or restricted for export as baggage?

All the passengers leaving India by air are subject to

clearance by Custom Authorities. Only

bona fide baggage is

allowed to be cleared by passengers. There is a procedure prescribed whereby

the passengers leaving India can take the export certificate for the various

high value items as well as jewellery from the Customs authorities. Such an

export certificate comes handy while bringing back the things to India so

that no duty is charged on such goods exported by the passenger.

Other information:

-

Export of most species of wild life and articles

made from wild flora and fauna, such as ivory, musk, reptile skins, furs, shahtoos, etc. is prohibited.

-

Trafficking of narcotic drugs and psychotropic

substances is prohibited.

-

Export of goods purchased against foreign exchange

brought in by foreign passengers are allowed except for prohibited goods.

-

Carrying of Indian currency notes in the

denomination of

500 and 1,000 to Nepal is prohibited.

Q.31 What are the requirements for export of gold jewellery

through baggage?

There is no value limit on the export of gold jewellery

by a passenger through the medium of baggage so long as it constitutes the

bona fide baggage of the passenger. A passenger may request the Customs for

issue of an export certificate at the time of his/her departure from India,

in respect of jewellery carried by him/her to facilitate its re-import

subsequently.

Commercial export of gold jewellery through the courier

mode is permitted subject to observance of prescribed procedures.

Q.32 Is export of foreign currency & Indian currency

permissible and if so to what extent?

While leaving India, tourists are allowed to take with

them foreign currency not exceeding an amount brought in by them at the time

of their arrival in India. As no declaration is required to be made for

bringing in foreign exchange/currency not exceeding equivalent of U.S. $

10,000, generally tourists can take out of India with them at the time of

their departure foreign exchange/currency not exceeding the above amount.

The export of foreign currency is otherwise prohibited.

Export of Indian currency is strictly prohibited. However

Indian residents when they go abroad are allowed to take with them Indian

currency not exceeding 7,500.

Chapter 7

RESTRICTED AND PROHIBITED GOODS

Q.33 Which are the restricted and prohibited goods for

import and/or export?

Certain goods are prohibited (banned) or restricted

(subject to certain conditions) for import and/or export. These are goods of

social, health, environment, wildlife and security concerns. Export or

import in prohibited and restricted goods commonly leads to arrest. Some

common examples of such goods are:

Prohibited Goods

-

Narcotic Drugs and Psychotropic substances

-

Pornographic material

-

Counterfeit and pirated goods and good infringing

any of the legally enforceable intellectual property rights

-

Antiquities

Restricted Goods

-

Firearms and ammunition

-

Live birds and animals including pets

-

Plants and their produce e.g. fruits, seeds

-

Endangered species of plants and animals, whether

live or dead

-

Any goods for commercial purpose: for profit, gain

or commercial usage

-

Radio transmitters not approved for normal usage

-

Gold and silver, other than ornaments (for import

only)

-

Indian and foreign currency in excess of

prescribed limits:

- foreign currency in form of currency notes in

excess of US$ 5000 or equivalent and foreign currency in the form of

currency notes, bank notes or travelers cheques in excess of US$ 10000

or equivalent is required to be declared on arrival.

- foreign currency in excess of amount legally

obtained or in the case of tourists in excess of the amount declared

on arrival or in excess of the exempted limit of declaration at the

time of departure.

-

Trafficking in Narcotic Drugs like Heroin, Charas,

Cocaine or in Psychotropic substances is a serious offence and is

punishable with imprisonment.

-

Export of most species of wild life and articles

made from flora and fauna such as Ivory, Musk, Reptile skins, Furs, Shahtoosh, etc. is prohibited. For any clarifications passenger should

approach the Regional Deputy Director (Wildlife Preservation) Govt. of

India or the Chief Wildlife Wardens of State Governments posted at Kolkata,

Delhi, Mumbai and Chennai.

Chapter 8

VIOLATIONS AND PENAL PROVISIONS

Q.34 Describe the different types of violations of customs

laws and the penal provisions that would be attracted?

The Indian Customs Act empowers imposition of heavy

penalties for those passengers who:

-

attempt to walk through the Green Channel with

prohibited, restricted or dutiable goods;

mis-declare their goods at the Red Channel;

attempt to export prohibited or restricted goods;

abet the commission of any of the above offences.

The penal provisions relating to searches, seizure and

arrest are covered in sections 100 to 110 of Chapter XIII of the Customs

Act, 1962. Penal provisions relating to confiscation of goods and imposition

of penalties are covered in sections 111 to 127 of Chapter XIV of the

Customs Act, 1962. Accordingly, penal provisions may lead to:

-

absolute confiscation of goods, or

-

imposition of heavy fine in respect of the

concerned goods if these are released;

-

imposition of penalty on individual or concerned

entities up to five times the value of goods or the duty involved

-

arrest and prosecution including invocation of

preventive detention in serious cases.

Chapter 9

REFERENCES

-

A Handbook on FEMA – Taxation by All India Federation

of Tax Practitioners

-

Baggage Rules of India (Sept. 2010 edn.) by P. Veera

Reddy & P. Mamatha

-

http://www.cbec.gov.in/customs/cs-act/formatted-htmls/

cs-reulf.htm

-

http://www.cbec.gov.in/travellers.htm

-

http://www.mumbaicustoms3.gov.in/htmldocs/tr.htm

Chapter 10

SUBJECT INDEX

|

Particulars |

Section/Notification |

Q. No.

|

|

Airline crew baggage |

Rule 10

|

Q.28

|

|

Alcoholic Drinks import

|

|

Q.19

|

|

Baggage |

|

Q.1

|

|

Bona fide Baggage

|

S. 79

|

Q.1

|

|

Carrier

|

|

Q.5

|

|

Cigarettes import

|

|

Q.19

|

|

Clearance of Baggage |

|

Q.7

|

|

Commercial Goods |

|

Q.6

|

|

Commercial Samples

|

|

Q.17

|

|

Consumer Goods |

|

Q.3

|

|

Customs Act, 1962

|

S. 77

to S. 81

|

Q.8

|

|

Customs Rate of Duty

|

|

Q.29

|

|

Deceased person’s baggage |

|

Q.25 |

|

Declaration of Baggage

|

S. 77

|

Q.7

|

|

Duty

free allowances

|

Rules

3, 4

|

Q.11 |

|

Family

|

2(iv)

|

Q.9

|

|

Fire

Arms import

|

|

Q.23 |

|

Foreign Exchange/Currency export

|

|

Q.32 |

|

Foreign Exchange/Currency import

|

|

Q.22 |

|

Foreign Nationals

|

|

Q.16 |

|

Gifts

/ Souvenirs |

|

Q.2,

Q.18

|

|

Gold

import

|

|

Q.21 |

|

Gold jewellery

export

|

|

Q.31 |

|

Green

Channel

|

|

Q.7 |

|

Indian Currency export |

|

Q.32 |

|

Indian Currency import

|

|

Q.22 |

|

Jewellery

import

|

Rule

6

|

Q.20 |

|

Laptop import

|

|

Q.11,

Q.28 |

|

Licence

for import

|

|

Q.4 |

|

Out-bound passengers |

|

Q.30 |

|

Passenger car import

|

|

Q.27 |

|

Passenger categories

|

|

Q.10 |

|

Pet

animals import

|

|

Q.24 |

|

Professional Equipment

|

2(v)

|

Q.9 |

|

Professionals

|

Rules

3, 4, 5

|

Q.12

|

|

Resident

|

2(ii)

|

Q.9

|

|

Restricted and prohibited Goods

|

|

Q.33

|

|

Silver import

|

|

Q.21

|

|

Tourist

|

2(iii), Rule 7

|

Q.9,

Q.13

|

|

Transfer of Residence

(TR)

Rules 3 |

4, 8

|

Q.14

|

|

Unaccompanied baggage

|

|

Q.26 |

|

Violations and Penal provisions

|

Ss.100 to 127 |

Q.34 |

|