![]()

![]()

![]()

![]()

|

|

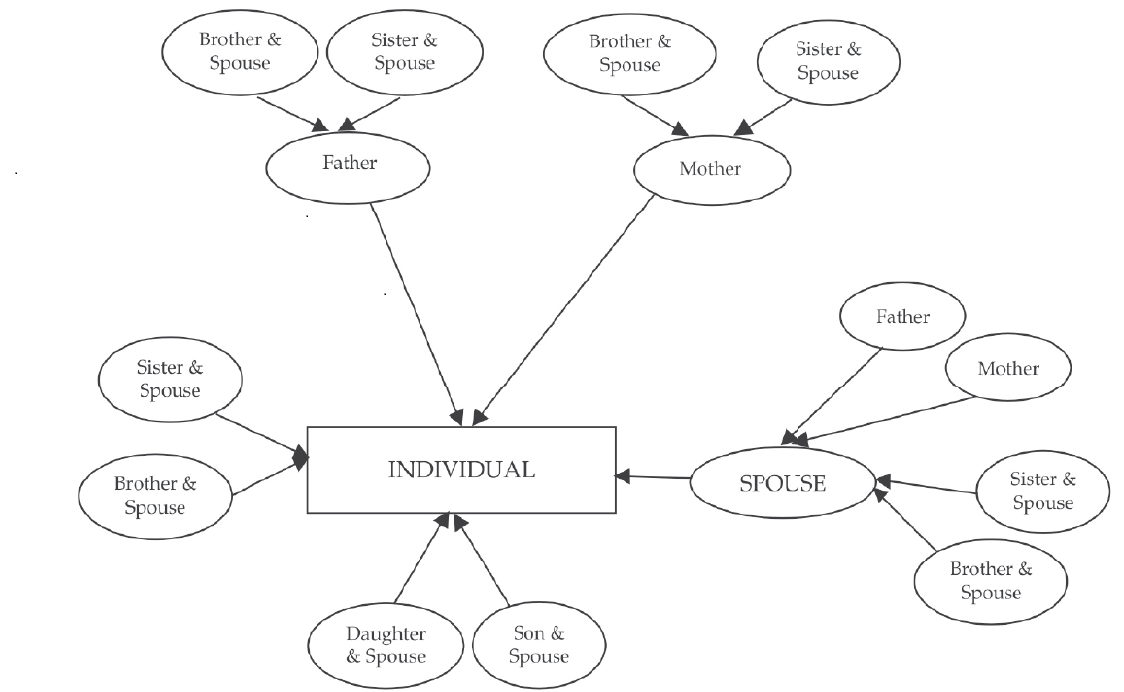

Generally, gifts received are not regarded as Income chargeable to Tax. However, by virtue of section 2(24)(xiii) r.w.s. 56(2)(v) after 1-9-2004 any sum of money exceeding Rs. 50,000 received without consideration by an individual or an HUF from any person is chargeable to tax as Income under the head Other Sources, subject to following exceptions: (a) Receipts from certain relatives; as defined in the section. (Refer Chart) (b) Receipts on occasion of marriage of the individual. (c) Receipts under a will or inheritance. (d) Receipts in contemplation of death of the payer. Sec. 56(2)(v) has been amended by the Taxation Laws (Amendment) Act, 2006 so as to exempt also the receipts from (i) local authority, (ii) institutions exempt u/s. 10(23C) and (iii) trusts/institutions registered u/s. 12AA. Sec. 56(2) has been further amended and w.e.f. 1-10-2009, the scope of gift is increased by adding immovable property or any property besides sum of money [S. 56(2)(vii)] excluding stock-in-trade, raw material, consumable stores or any other trading assets as under: List of Property –

Valuation of Gift in case of

(a) without consideration – if stamp duty value exceeds ` 50,000/-, stamp duty value (b) for a consideration which is less than stamp duty value – if the stamp duty value exceeds the consideration by ` 50,000/-, stamp duty value less consideration (w.e.f. A.Y. 2014-15)

It is also

provided that in a case where the date of the agreement to purchase the property

fixing the consideration and the date of registration are different, the taxability

will be determined with reference to the stamp duty value on the date of agreement

and not registration. This exception will apply only where at least part of the

consideration has been paid by any mode other than cash, on or before the date of

such agreement.

w.e.f. 1-6-2010 following items added:–

A. Provision not applicable in case of the following restructuring:

B. Receipt of shares of a closely-held company by a firm (including LLP) or a closely-held company taxable if transfer is without consideration or for inadequate consideration. C. Fair market value less consideration is taxable, subject to difference of more than Rs. 50,000. D. Amount taxed to be treated as cost of acquisition in the hands of recipient. Gift of more than Rs. 50,000/- can be received from

Notes:

Valuation rules for determining ‘fair market value of gifts’ Background The Finance (No. 2) Act, 2009 has inserted clause (vii) in section 56(2) of the Income-tax Act (‘the Act’) to tax an Individual or a Hindu Undivided Family (HUF) who is receiving any asset which is in the nature of shares and securities, jewellery, archaeological collections, drawings, paintings, sculptures or any work of art (specified assets) without consideration or for inadequate consideration i.e. consideration which is less than fair market value (FMV) by an amount exceeding Rs. 50,000. Further, the Finance Act, 2010 introduced similar provisions to tax receipt of shares of a closely-held company by a firm or another closely held company w. e. f. 1-6-2010. For the purpose of determining fair market value, Rules 11U and 11UA were introduced. With the applicability of the Act, Rules are also applied accordingly. Synopsis of the Rules The rules 11U and 11UA prescribes the different methods for the purpose of valuation of specified assets. The FMV of the specified asset needs to be determined on a date on which such specified assets are received by the assessee. The determination of FMV, under this rule, will be only for the purpose of section 56 of the Act. Notification No. 23/ 2010, which came into force from 1st October, 2009. Further, specified assets received from relative are not covered by the provisions of Section 56(2)(vii) of the Act. Methods of Valuation 1. Valuation of specified assets (other than shares & securities)

2. Valuation of Shares & Securities

Applicable w.e.f. A.Y.2013-14 Sec 56(2)viib) applies to Closely held company : Where a closely held company receives any consideration from resident person for issue of shares that exceeds the face value of shares, then the consideration received in excess of the fair market value of the shares shall be taxable under the head Income from other sources.

Retrospective amendment for gifts received by HUF : Any sum or property received without consideration or inadequate consideration by HUF from its members would also be excluded from taxation. w.e.f. 1-10-2009 [Refer amendment made to sec. 56(2)(vii)] |

|

|